Switzerland, one of the most important global financial centers and home to more than 250 banks, is actually a small of nation of 8 million people, that you may associate with world class chocolate, luxurious watches, the stunning scenery of the Alps and lakes, as well as excellent education infrastructure and unrivaled living standards. All these things and more, but probably not fintech. At least, not yet.

The financial services industry has always been, and still is, of essential importance to the Swiss economy. This is an industry that added about $80 billion for the national economy in 2014, according to the Swiss Bankers Association.

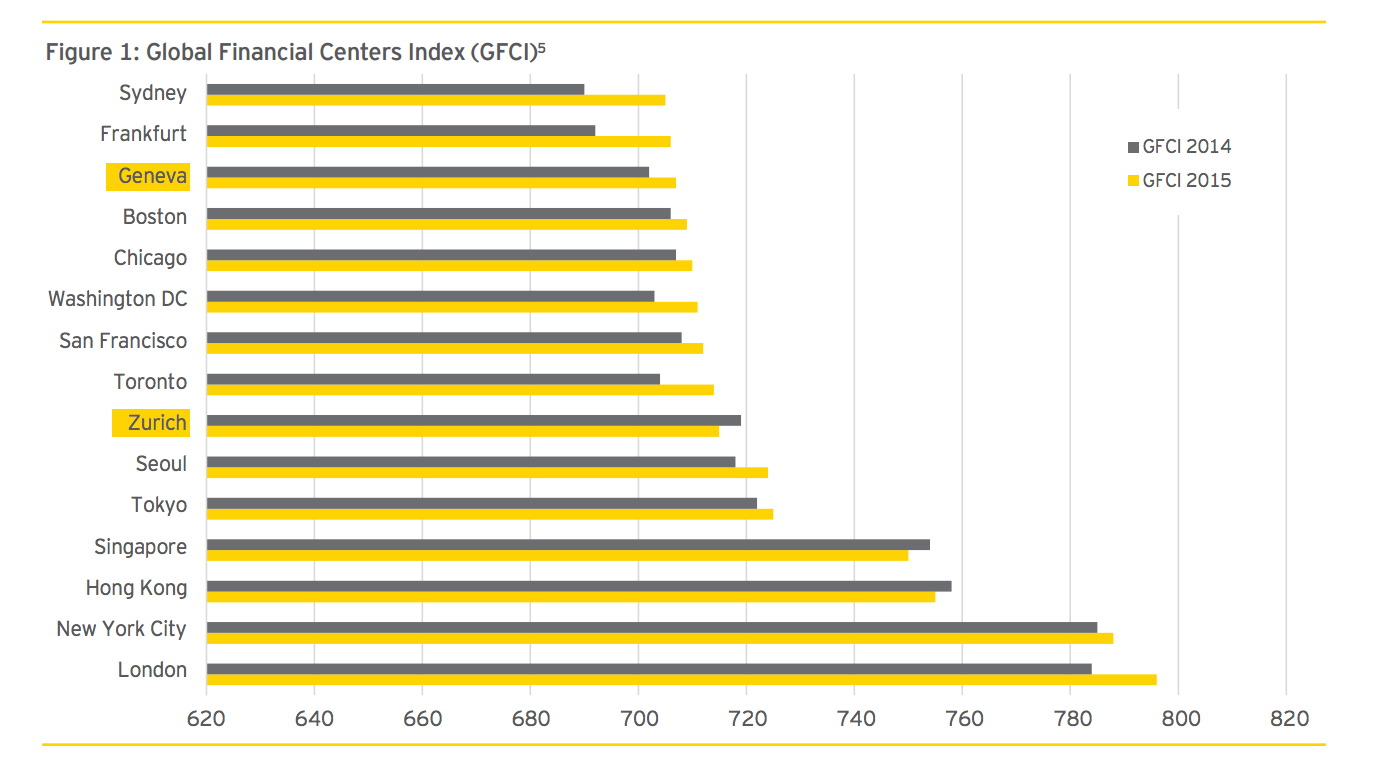

Until a few years ago, Banking Secrecy was one of the main characteristics and key factors in the rise of the Swiss financial ecosystem, which boast not one but two cities considered among the top financial centers of the world (see chart below). According to the Global Financial Centers Index (GFCI), Zurich occupies the seventh position in the world, and it’s in the second position, just after London, in Europe. But a few places down, in 13th position, is another city flying the Swiss colors; Geneva.

Until a few years ago, Banking Secrecy was one of the main characteristics and key factors in the rise of the Swiss financial ecosystem, which boast not one but two cities considered among the top financial centers of the world (see chart below). According to the Global Financial Centers Index (GFCI), Zurich occupies the seventh position in the world, and it’s in the second position, just after London, in Europe. But a few places down, in 13th position, is another city flying the Swiss colors; Geneva.

(Source: The Global Innovation Index 2015 report, as showed on the EY Swiss Fintech Report 2016)

Considering the loss of banking secrecy and the major commitment to technological development in other financial centers, like London, Singapore and New York, it is quintessential for Switzerland to adapt and innovate if the country wants to maintain the importance gained in the last century as a key financial center. The Swiss government and regulators are now trying to fill that gap with a package of new measures, approved on the 2nd of November, 2016 including what has been called a FinTech license. This license will simplify regulations for financial technology firms relative to those heavy requirements placed on banks and financial institutions. The package also includes a fintech sandbox, allowing companies to test new technologies in a safe space, as well as measures to boost crowdfunding. Let’s now look at it in more detail.

What’s this license for fintech firms all about?

FinTech firms, with a minimum of 300,000 Swiss Francs (~ $297k) in capital, will be allowed to accept funds from clients, up to 100 million Swiss Francs (~ $99m) which remain outside the depositor protection scheme and are not subject to the same regulations, auditing and the capital requirements applied to banks. However the eligible Swiss financial technology companies won’t be able to make long-term loans, which remains exclusively for banks.

What changes are in store for online investing and crowdfunding platforms?

The Swiss government has proposed to set a period of 60 days, where crowdfunding platform operators will be able to hold money from investors in settlement accounts. The government is also willing to remove the limit on the maximum number of people that can invest in a single fundraiser on a crowdfunding platform, with the current limit being 20. By removing the limit, it will be possible to have an unlimited number of investors participating in a fundraise through crowdfunding.

Mark Branson, CEO of the Swiss Financial Market Supervisory Authority (FINMA), told the Financial Times that they “want to create one tailor-made license category for all kinds of innovative financial players — which is not something that has been done anywhere else in the world,”. While Ueli Maurer, the Swiss finance minister, who was already labelled as Mr. Fintech, emerged as Switzerland's main fintech industry promoter, said to journalists that “Fintech is going to be an important element of our financial marketplace strategy,” and that they “want in the future to belong to the most important financial centres in this sector,”.

Considering the loss of banking secrecy and the major commitment to technological development in other financial centers, like London, Singapore and New York, it is quintessential for Switzerland to adapt and innovate if the country wants to maintain the importance gained in the last century as a key financial center. The Swiss government and regulators are now trying to fill that gap with a package of new measures, approved on the 2nd of November, 2016 including what has been called a FinTech license. This license will simplify regulations for financial technology firms relative to those heavy requirements placed on banks and financial institutions. The package also includes a fintech sandbox, allowing companies to test new technologies in a safe space, as well as measures to boost crowdfunding. Let’s now look at it in more detail.

What’s this license for fintech firms all about?

FinTech firms, with a minimum of 300,000 Swiss Francs (~ $297k) in capital, will be allowed to accept funds from clients, up to 100 million Swiss Francs (~ $99m) which remain outside the depositor protection scheme and are not subject to the same regulations, auditing and the capital requirements applied to banks. However the eligible Swiss financial technology companies won’t be able to make long-term loans, which remains exclusively for banks.

What changes are in store for online investing and crowdfunding platforms?

The Swiss government has proposed to set a period of 60 days, where crowdfunding platform operators will be able to hold money from investors in settlement accounts. The government is also willing to remove the limit on the maximum number of people that can invest in a single fundraiser on a crowdfunding platform, with the current limit being 20. By removing the limit, it will be possible to have an unlimited number of investors participating in a fundraise through crowdfunding.

Mark Branson, CEO of the Swiss Financial Market Supervisory Authority (FINMA), told the Financial Times that they “want to create one tailor-made license category for all kinds of innovative financial players — which is not something that has been done anywhere else in the world,”. While Ueli Maurer, the Swiss finance minister, who was already labelled as Mr. Fintech, emerged as Switzerland's main fintech industry promoter, said to journalists that “Fintech is going to be an important element of our financial marketplace strategy,” and that they “want in the future to belong to the most important financial centres in this sector,”.

(Source: The Global Innovation Index 2015 report, as showed on the EY Swiss Fintech Report 2016)

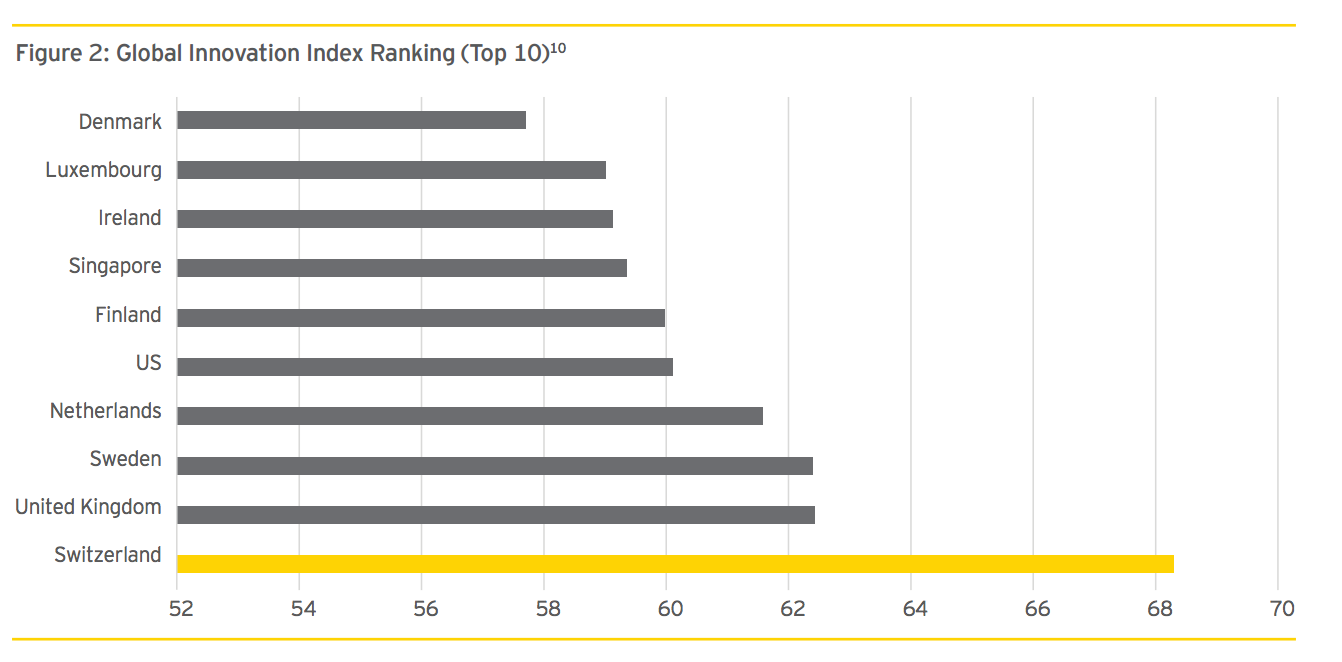

Switzerland could be late on fintech but that is certainly not the case on overall innovation. The Global Innovation Index, prepared by INSEAD Business School, Cornell University and WIPO (World Intellectual Property Organization), ranked the country as the world's most innovative country since 2011, excelling in particular with its research systems and SMEs in-house innovation.

Considering the strategic position of the country in Europe, both geographically and complemented by Zurich and Geneva as international financial centers, along with the new regulations and measures proposed to stimulate financial innovation, the fintech industry in Switzerland seems to have finally arrived and is poised to take advantage of excellent opportunities in the foreseeable future. If you’re interested in jumping into it before it’s too late, all you need to do is to contact us and we'll be glad to assist your entry into the Swiss FinTech ecosystem.

Switzerland could be late on fintech but that is certainly not the case on overall innovation. The Global Innovation Index, prepared by INSEAD Business School, Cornell University and WIPO (World Intellectual Property Organization), ranked the country as the world's most innovative country since 2011, excelling in particular with its research systems and SMEs in-house innovation.

Considering the strategic position of the country in Europe, both geographically and complemented by Zurich and Geneva as international financial centers, along with the new regulations and measures proposed to stimulate financial innovation, the fintech industry in Switzerland seems to have finally arrived and is poised to take advantage of excellent opportunities in the foreseeable future. If you’re interested in jumping into it before it’s too late, all you need to do is to contact us and we'll be glad to assist your entry into the Swiss FinTech ecosystem.

About the author - Alessandro Ravanetti

Alessandro is Co-founder & CMO of Crowd Valley. He has worked in the fintech industry, with marketplace investing and lending, since 2011. Has built and managed digital companies with distributed teams and international partners, and gained experience with both startups and large corporations, having worked with British Telecom, Bloomberg and the Grow VC Group.

Alessandro grew up in Italy, where he graduated with a B.A. in Economics at University of Parma, before to obtain a M.S. in Finance at Regent’s University London. He studied and worked in many different cities, including Munich, Geneva, London, Barcelona and Valencia. Genuinely passionate about financial technology and innovation, he loves to spend his spare time traveling and discovering new cultures. You can find him on Twitter at @aleravanetti.

Alessandro is Co-founder & CMO of Crowd Valley. He has worked in the fintech industry, with marketplace investing and lending, since 2011. Has built and managed digital companies with distributed teams and international partners, and gained experience with both startups and large corporations, having worked with British Telecom, Bloomberg and the Grow VC Group.

Alessandro grew up in Italy, where he graduated with a B.A. in Economics at University of Parma, before to obtain a M.S. in Finance at Regent’s University London. He studied and worked in many different cities, including Munich, Geneva, London, Barcelona and Valencia. Genuinely passionate about financial technology and innovation, he loves to spend his spare time traveling and discovering new cultures. You can find him on Twitter at @aleravanetti.

RSS Feed

RSS Feed