On November 10, 2016, the UK and China announced a joint initiative to provide their domestic investors with new investment opportunities while further opening their respective markets to foreign capital. Named the London-Shanghai Stock Connect, it focuses on eight key areas and ultimately aims at easing cooperation and boosting market access. Those areas range from traditional sectors such as banking and asset management but also include socially important ones, for instance financial inclusion or green finance.

Another area of interest for the signatories is financial technology, better known as fintech. Indeed, an agreement was signed between the People’s Bank of China and UK’s Financial Conduct Authority in order to establish a UK-China Fintech Bridge. In the words of Andrew Bailey, Chief Executive of the FCA: “The Co-operation Agreement will allow us to share information about financial services innovations in our respective markets, including emerging trends and regulatory issues”.

Source: Harnessing Potential: The Asia-Pacific Alternative Finance Benchmarking Report by Cambridge Center for Alternative Finance and the University of Sydney Business School.

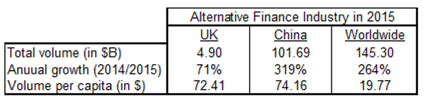

Both the British and Chinese fintech markets are already recognized as major hubs within the alternative finance industry. But where the former is known to be a magnet for actors aiming at entering Europe, the latter relies more heavily on the unmatchable depth of its domestic market (that accounts for almost 70% of the global volume according to a recent report by KPMG and the Cambridge Center for Alternative Finance). Size-wise, the Chinese alternative finance industry was more than 20 times bigger than the British one in 2015, and even grew 4.5 times faster compared to the previous year’s levels. However, when adjusting those figures to reflect the average volume per inhabitant, both volumes per capita are almost identical. Ranked #2 (China with $74.16 per capita) and #3 (UK with $72.41 per capita) worldwide, UK and China are still far away from the US level ($112.14 per capita) but also far ahead from the rest of the globe (4th place is New Zealand, with $58.27 per capita).

Source: Global insights from regional Alternative Finance studies, KPMG & Cambridge Center for Alternative Finance.

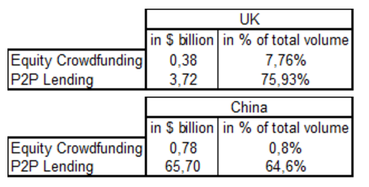

When comparing the respective size of different segments with the total volume, it appears that the British market is more driven by the equity crowdfunding and peer-to-peer lending sectors than the Chinese one:

Britain’s decision secede from the European Union leaves British fintech firms likely to face regulatory challenges due to ‘passporting’ limitations that may come into effect once the UK actually triggers Article 50 and completes their secession from the EU. This creates a window of opportunity for other European financial centres to establish themselves as major FinTech hubs as the attractiveness of London’s financial center possibly diminishes in the wake of Brexit.

Meanwhile, the Chinese alternative finance industry is thriving. Thousands of firms are aiming at providing innovative solutions to the country’s 1.3 billion inhabitants, and they are often backed by the government in this endeavor. Those circumstances led to the creation of fintech giants, but today even the world’s most populated country seems too small to ensure those firms a sustainable growth.

In light of this, the agreement that was reached between the two countries illustrates the need for cross-border collaboration in order to harmonize the business models and regulatory requirements worldwide. Likewise, the increasing involvement of institutional actors seems to be paving the way for globalization of the alternative finance industry.

Thanks to its global presence and international partners, Crowd Valley is closely following ongoing evolutions within the global alternative finance landscape. And any party interested in providing digital solutions with the help of our cutting-edge financial technology can reach out to us via our contact form.

Meanwhile, the Chinese alternative finance industry is thriving. Thousands of firms are aiming at providing innovative solutions to the country’s 1.3 billion inhabitants, and they are often backed by the government in this endeavor. Those circumstances led to the creation of fintech giants, but today even the world’s most populated country seems too small to ensure those firms a sustainable growth.

In light of this, the agreement that was reached between the two countries illustrates the need for cross-border collaboration in order to harmonize the business models and regulatory requirements worldwide. Likewise, the increasing involvement of institutional actors seems to be paving the way for globalization of the alternative finance industry.

Thanks to its global presence and international partners, Crowd Valley is closely following ongoing evolutions within the global alternative finance landscape. And any party interested in providing digital solutions with the help of our cutting-edge financial technology can reach out to us via our contact form.

About the author - Enzo Ramos

Born and raised in France, Enzo began working within Fintech in 2014, covering the regulatory changes than enabled the creation of French equity crowdfunding platforms for Lyon Place Financière, an association that regroups all actors of Auvergne-Rhône-Alpes’ financial place. There, he also worked on an exhaustive analysis of the regional stock market among other duties. Enzo has lived and studied in different countries, including the United States (Philadelphia & Monroe,MI) and France (Paris & Lyon).

Born and raised in France, Enzo began working within Fintech in 2014, covering the regulatory changes than enabled the creation of French equity crowdfunding platforms for Lyon Place Financière, an association that regroups all actors of Auvergne-Rhône-Alpes’ financial place. There, he also worked on an exhaustive analysis of the regional stock market among other duties. Enzo has lived and studied in different countries, including the United States (Philadelphia & Monroe,MI) and France (Paris & Lyon).

RSS Feed

RSS Feed