With its high GDP, 2nd highest e-commerce volume in Asia and high rate of technological adoption, Japan presents a high potential for Fintech investment and adoption. However, the uptake has been lukewarm so far, owing to significant cultural and regulatory obstacles with Japanese investments accounted for only 0.40 percent of the roughly US$12 billion invested into Fintech globally in 2014, according to a report by Accenture.

However, with efforts being made by incumbents and the FSA, 2017 is poised to be a potentially mercurial year for Japanese Fintech with the 2020 Tokyo Olympics representing a key trigger to accelerate legal revision and inject momentum into the Fintech industry.

With the West continuing to display consistent growth and adoption of financial technology, there are significant changes afoot within the institutional and regulatory framework to act as catalysts for Japanese Fintech growth. The changes are part of a national effort to push financial technology, highlighting fears in Tokyo that Silicon Valley could damage Japan’s banking sector as it did the country’s mobile phone industry in the past. “Japanese institutions are concerned that a Google Bank or Facebook Bank will conquer Japan,” said Naoyuki Iwashita, head of the Fintech Centre at the Bank of Japan. It also means that Japan could become a big new source of capital for startups, especially in Asia, that are experimenting with technologies such as Blockchain or Artificial Intelligence. Yasuhiro Sato, Chief Executive of Mizuho told a conference in Tokyo in October 2016 that Japanese banks had been constrained by regulators wanting to preserve old, but tried and tested, IT systems.

IT investments by Japanese financial groups have historically stagnated at around 3%, a level well below their global peers. This can partly be explained by the lack of support towards innovation from senior management, and, most importantly, by the legal limitation on banks’ IT investments.

Until recently, the Banking Act prevent Japanese banks from having a stake higher than 5% stake in an non- finance-based company, limiting them from investing heavily in Fintech startups. Taro Aso, Deputy Prime Minister, suggested that some of the same spirit from the West needed to be instilled in Tokyo. “We have revised the Banking Act and, through the revision, people in banks, in business suits work together with young people in T-shirts and jeans. They work together and the combination of this gives rise to new things.” He added: “The financial ministry which used to regulate the industry must now nurture the industry. We are making efforts towards this end. We haven’t done enough but with this new policy we have greatly changed our thinking in approaching the issues.”

Beyond the Banking Act, Japan has also taken other steps forward, like recently legislating to regulate digital currency exchanges in the country and establishing a number of working groups involving the Bank of Japan and the Ministry of Finance. But there is still a lot of bureaucracy to get through in order to launch and grow a new company.

With the West continuing to display consistent growth and adoption of financial technology, there are significant changes afoot within the institutional and regulatory framework to act as catalysts for Japanese Fintech growth. The changes are part of a national effort to push financial technology, highlighting fears in Tokyo that Silicon Valley could damage Japan’s banking sector as it did the country’s mobile phone industry in the past. “Japanese institutions are concerned that a Google Bank or Facebook Bank will conquer Japan,” said Naoyuki Iwashita, head of the Fintech Centre at the Bank of Japan. It also means that Japan could become a big new source of capital for startups, especially in Asia, that are experimenting with technologies such as Blockchain or Artificial Intelligence. Yasuhiro Sato, Chief Executive of Mizuho told a conference in Tokyo in October 2016 that Japanese banks had been constrained by regulators wanting to preserve old, but tried and tested, IT systems.

IT investments by Japanese financial groups have historically stagnated at around 3%, a level well below their global peers. This can partly be explained by the lack of support towards innovation from senior management, and, most importantly, by the legal limitation on banks’ IT investments.

Until recently, the Banking Act prevent Japanese banks from having a stake higher than 5% stake in an non- finance-based company, limiting them from investing heavily in Fintech startups. Taro Aso, Deputy Prime Minister, suggested that some of the same spirit from the West needed to be instilled in Tokyo. “We have revised the Banking Act and, through the revision, people in banks, in business suits work together with young people in T-shirts and jeans. They work together and the combination of this gives rise to new things.” He added: “The financial ministry which used to regulate the industry must now nurture the industry. We are making efforts towards this end. We haven’t done enough but with this new policy we have greatly changed our thinking in approaching the issues.”

Beyond the Banking Act, Japan has also taken other steps forward, like recently legislating to regulate digital currency exchanges in the country and establishing a number of working groups involving the Bank of Japan and the Ministry of Finance. But there is still a lot of bureaucracy to get through in order to launch and grow a new company.

Image Source: Fintech Market Report by Accenture (2015).

Image Source: Fintech Market Report by Accenture (2015).

Image Source: Fintech Market Report by Accenture (2015). Lack of mobility in the workforce is another problem that Japan shares with other countries, including Singapore. “A lot of very smart people prefer to work for large companies where there’s stable work and a good salary versus working at a startup,” said Natalie Shiori Fleming during a keynote speech at Tech in Asia Tokyo 2016. Natalie leads US financial services company Payoneer’s regulatory and banking infrastructure strategy in the Japan.

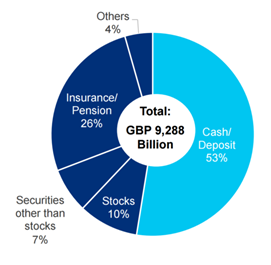

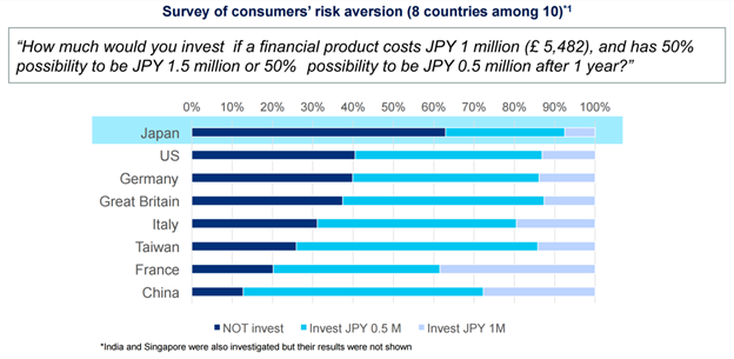

The regulatory environment in Japan ties in closely with the prevalent culture towards banking and investment. Traditionally, Japanese people have been seen as risk averse with regards to banking and investment practices. Over 52% of personal assets are composed of cash and deposits, with 0% interest. This is complemented by a lack of financial literacy that hinders investment and makes it harder for Fintech services in the wealth management and investment sectors to grow.

The regulatory environment in Japan ties in closely with the prevalent culture towards banking and investment. Traditionally, Japanese people have been seen as risk averse with regards to banking and investment practices. Over 52% of personal assets are composed of cash and deposits, with 0% interest. This is complemented by a lack of financial literacy that hinders investment and makes it harder for Fintech services in the wealth management and investment sectors to grow.

Furthermore, trust plays a huge role in Japan and this cultural characteristic is strongly reflected in the strict regulatory environment as well as in a strong inclination to abide by law in all aspects which contrasts with the attitude seen in the Fintech-embracing-West where startups and incumbents both look to innovate and push the limits of the legal system in their bid for innovation and transformation. Japanese also view their security and privacy very seriously. There are strict rules on how customer data can be handled and an upcoming amendment to the Personal Information Protection Act will place further burden on private data holders.

A poll by the Japanese Bankers Association gives insight into these concerns and shows the number one reason people chose not to use online banking is security fears.

A poll by the Japanese Bankers Association gives insight into these concerns and shows the number one reason people chose not to use online banking is security fears.

Image Source: Fintech Market Report by Accenture (2015).

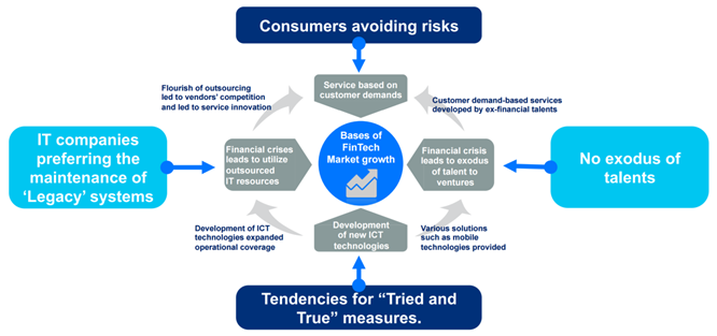

This same trust is seen in the massive banking system in Japan. While Fintech is certainly growing in the country, it appears the reason it hasn’t taken off so quickly is partly due to a strong bank-branch culture. The Data Market has found that the number of commercial bank branches per 1,000 square kilometres in Japan in 2013 was 103. This is significantly higher than those found in the rest of Asia.

In this regard, one interesting perspective is that the Japanese are too satisfied with their banks. This isn’t a statement you associate with a problem, but the issue there for Fintech businesses is that there is less dissatisfaction with traditional financial services in Japan than there is in other parts of the world like the US and the UK. The Japanese are less likely to want to look for a different service that will better meet their needs. This dissatisfaction within the consumer base was a major catalyst for Fintech and startup culture in the West. Unlike the banking systems in the EU and especially, the U.S., the banking system in Japan did not undergo significant decimation with the global recession and actually managed to keep the damage to its consumer base at a relative minimum. At the same time in the West, there was a significant exodus of talent and entrepreneurs exiting financial institutions and fueling the alternative finance and startup culture that is thriving in the West. The 2008 financial crisis brought about a complete change in mindset and regulatory environment for the western world but in an environment that didn’t experience the same damage and dissatisfaction, Fintech faces the obstacle of answering the question:

“Why deviate from tried and tested systems?”

One of the other minor factors in a slow Fintech adoption rate in Japan is the hacking at the now defunct Tokyo-based Mt. Gox. Founded in 2010 and run by Mark Karpeles, in 2014 it was reported that around 850,000 bitcoins belonging to customers and the company went missing. It is believed that the missing bitcoin were stolen over time from the Mt. Gox hot wallet from 2011. However, considering that of all financial technology developments, bitcoin is one of the leaders in digital transformation, the extent to which Mt. Gox continues to play a role is questionable.

Ripple, the US Fintech that uses Blockchain technology for payments and settlement, has entered into a joint venture in January, 2016 with Japanese financial services giant SBI Holdings. It's called SBI Ripple Asia, and in August 2016, it was announced that a consortium of 15 Japanese banks, will build a platform using Ripple technology to enable instant national and cross-border payments. It plans to expand the consortium to 30 banks and launch the service in spring 2017.

The number of merchants accepting the cryptocurrency is expected to quintuple to 20,000 this year. By 2016’s end, there were over 4,200 bitcoin-accepting merchants and storefronts in the country, quadrupling from the total from 2015. The frenetic growth followed a bill, approved by the Japanese cabinet, to recognize digital currencies as real money, or legal tender.

CoinCheck’s chief of business development Kagayaki Kawabata points to Japan’s regulatory moves as the primary factor for bitcoin’s growing popularity in the country. Once shunned in a negative light during the fallout of the now-defunct Mt. Gox exchange, the cryptocurrency is seeing plenty of press that is helping spread awareness in the country.

Scheduled to take place in Spring 2017, the regulatory bill is, in essence, a legislative revision to the fund settlement law. Originally, the law did not recognize bitcoin and digital currencies as equivalents to conventional currencies. The amendment will deem bitcoin to have “asset-like values” to make it legal as tender with payments or with transfers as an asset. Further, bitcoin is increasingly being seen as a transactional currency in its duality as an investment or store of value.

An excerpt from Nikkei’s report points to yet another factor that could see a massive wave of publicity and adoption of bitcoin in the country.

Unlike national currencies, it [bitcoin] transcends borders without the need for exchange. It may behoove Japan, as host of the 2020 summer Olympics, to cater to foreigners paying in bitcoin.

While the cryptocurrency has been growing in popularity, the same cannot be said of other sectors conventionally linked to Fintech, more specifically business and P2P Lending which can be partly attributed to the earlier discussed risk averse and cash heavy culture but also to the long standing deflation. Japan’s economy has been experiencing deflation for almost 20 years, which has led to an unattractive environment for lending and business growth due to falling profits and reduced consumer demand across all sectors. This poses a serious obstacle for a number of global Fintech businesses such as P2P and P2B lending which are witnessing mercurial growth in the West. This deflation environment thus does not strongly or easily support new business growth and innovation with the global entrepreneurship monitor reporting that Japan has the 2nd lowest rank globally for early entrepreneurial activity. The push for Fintech innovation and collaboration thus has to come from the cash rich banking conglomerates and from deregulation, both of which have seen positive developments in recent years.

Mitsubishi UFJ Financial Group and the two other Japanese megabanks have been laying the groundwork ahead of the rules change, such as establishing dedicated divisions and launching contests designed to unearth promising startups. The legislation's passage opens the door to full-fledged investments and tie-ups. Sumitomo Mitsui Financial Group is interested in operating a virtual marketplace much like Rakuten's.

The potential in the market is there to achieve; a report by research firm Yano ICT that expects local Fintech market sales to grow ninefold in the next four years, from US$33.6 million in 2015 to US$563 million. Japan’s Mizuho is the latest banking giant to set up an innovation lab as it bids to nurture a Fintech ecosystem and build up relationships with startups. The lab will be based at Tokyo Finolab, a Fintech centre in the financial district backed by Real Estate giant Mitsubishi Estate and advertising firm Dentsu. The bank will invite firms to carry out technical trials of new services based on the development environment of its soon-to-launch Open Bank API. By combining Mizuho’s customer base and financial services expertise, with Metaps’ data analysis tech and WiL’s access to startups, the partners hope to develop payment services specifically for smartphones and explore how to harness data better and the use of Blockchain technology.

The rapid growth is in part due to the recent deregulation. In addition to the existing lending and funding types (‘Charity’, ’Rewards’ and ’Lending’), the ‘Equity-type’ market has emerged since 2015. Due to the contribution of this new funding type, we expect to see a further growth in the market with recent market trends expected to provide a boost to foreign players in entering the Japanese market and domestic players are likely to seek global partners to access overseas investors, technologies and ‘Equity-type’ knowledge.

This is going to be a big year for Japan. Is it heading towards its next financial data monopoly or an era of open APIs and blossoming startups? No one knows for sure, but Fintech is here to stay and we at Crowd Valley look forward to supporting your digital finance venture in Japan.

In this regard, one interesting perspective is that the Japanese are too satisfied with their banks. This isn’t a statement you associate with a problem, but the issue there for Fintech businesses is that there is less dissatisfaction with traditional financial services in Japan than there is in other parts of the world like the US and the UK. The Japanese are less likely to want to look for a different service that will better meet their needs. This dissatisfaction within the consumer base was a major catalyst for Fintech and startup culture in the West. Unlike the banking systems in the EU and especially, the U.S., the banking system in Japan did not undergo significant decimation with the global recession and actually managed to keep the damage to its consumer base at a relative minimum. At the same time in the West, there was a significant exodus of talent and entrepreneurs exiting financial institutions and fueling the alternative finance and startup culture that is thriving in the West. The 2008 financial crisis brought about a complete change in mindset and regulatory environment for the western world but in an environment that didn’t experience the same damage and dissatisfaction, Fintech faces the obstacle of answering the question:

“Why deviate from tried and tested systems?”

One of the other minor factors in a slow Fintech adoption rate in Japan is the hacking at the now defunct Tokyo-based Mt. Gox. Founded in 2010 and run by Mark Karpeles, in 2014 it was reported that around 850,000 bitcoins belonging to customers and the company went missing. It is believed that the missing bitcoin were stolen over time from the Mt. Gox hot wallet from 2011. However, considering that of all financial technology developments, bitcoin is one of the leaders in digital transformation, the extent to which Mt. Gox continues to play a role is questionable.

Ripple, the US Fintech that uses Blockchain technology for payments and settlement, has entered into a joint venture in January, 2016 with Japanese financial services giant SBI Holdings. It's called SBI Ripple Asia, and in August 2016, it was announced that a consortium of 15 Japanese banks, will build a platform using Ripple technology to enable instant national and cross-border payments. It plans to expand the consortium to 30 banks and launch the service in spring 2017.

The number of merchants accepting the cryptocurrency is expected to quintuple to 20,000 this year. By 2016’s end, there were over 4,200 bitcoin-accepting merchants and storefronts in the country, quadrupling from the total from 2015. The frenetic growth followed a bill, approved by the Japanese cabinet, to recognize digital currencies as real money, or legal tender.

CoinCheck’s chief of business development Kagayaki Kawabata points to Japan’s regulatory moves as the primary factor for bitcoin’s growing popularity in the country. Once shunned in a negative light during the fallout of the now-defunct Mt. Gox exchange, the cryptocurrency is seeing plenty of press that is helping spread awareness in the country.

Scheduled to take place in Spring 2017, the regulatory bill is, in essence, a legislative revision to the fund settlement law. Originally, the law did not recognize bitcoin and digital currencies as equivalents to conventional currencies. The amendment will deem bitcoin to have “asset-like values” to make it legal as tender with payments or with transfers as an asset. Further, bitcoin is increasingly being seen as a transactional currency in its duality as an investment or store of value.

An excerpt from Nikkei’s report points to yet another factor that could see a massive wave of publicity and adoption of bitcoin in the country.

Unlike national currencies, it [bitcoin] transcends borders without the need for exchange. It may behoove Japan, as host of the 2020 summer Olympics, to cater to foreigners paying in bitcoin.

While the cryptocurrency has been growing in popularity, the same cannot be said of other sectors conventionally linked to Fintech, more specifically business and P2P Lending which can be partly attributed to the earlier discussed risk averse and cash heavy culture but also to the long standing deflation. Japan’s economy has been experiencing deflation for almost 20 years, which has led to an unattractive environment for lending and business growth due to falling profits and reduced consumer demand across all sectors. This poses a serious obstacle for a number of global Fintech businesses such as P2P and P2B lending which are witnessing mercurial growth in the West. This deflation environment thus does not strongly or easily support new business growth and innovation with the global entrepreneurship monitor reporting that Japan has the 2nd lowest rank globally for early entrepreneurial activity. The push for Fintech innovation and collaboration thus has to come from the cash rich banking conglomerates and from deregulation, both of which have seen positive developments in recent years.

Mitsubishi UFJ Financial Group and the two other Japanese megabanks have been laying the groundwork ahead of the rules change, such as establishing dedicated divisions and launching contests designed to unearth promising startups. The legislation's passage opens the door to full-fledged investments and tie-ups. Sumitomo Mitsui Financial Group is interested in operating a virtual marketplace much like Rakuten's.

The potential in the market is there to achieve; a report by research firm Yano ICT that expects local Fintech market sales to grow ninefold in the next four years, from US$33.6 million in 2015 to US$563 million. Japan’s Mizuho is the latest banking giant to set up an innovation lab as it bids to nurture a Fintech ecosystem and build up relationships with startups. The lab will be based at Tokyo Finolab, a Fintech centre in the financial district backed by Real Estate giant Mitsubishi Estate and advertising firm Dentsu. The bank will invite firms to carry out technical trials of new services based on the development environment of its soon-to-launch Open Bank API. By combining Mizuho’s customer base and financial services expertise, with Metaps’ data analysis tech and WiL’s access to startups, the partners hope to develop payment services specifically for smartphones and explore how to harness data better and the use of Blockchain technology.

The rapid growth is in part due to the recent deregulation. In addition to the existing lending and funding types (‘Charity’, ’Rewards’ and ’Lending’), the ‘Equity-type’ market has emerged since 2015. Due to the contribution of this new funding type, we expect to see a further growth in the market with recent market trends expected to provide a boost to foreign players in entering the Japanese market and domestic players are likely to seek global partners to access overseas investors, technologies and ‘Equity-type’ knowledge.

This is going to be a big year for Japan. Is it heading towards its next financial data monopoly or an era of open APIs and blossoming startups? No one knows for sure, but Fintech is here to stay and we at Crowd Valley look forward to supporting your digital finance venture in Japan.

About the Author: Adit Vaddi

Adit Vaddi is a business development associate with a Bachelor of Arts in Economics from Vassar College, New York. He has a background in Economics, Accounting, Political Science and Operations (Event Management). He is from Hyderabad, India. Prior to Crowd Valley, Adit has worked as a research analyst for Baring's Private Equity Partners in Mumbai and for the IdeaSpace Foundation in Manila as well as a risk analyst for Fincare in Bangalore. On the operations side, Adit has organized and run over 30 large scale events that cater primarily to a college community. He is currently based in New York City.

Adit Vaddi is a business development associate with a Bachelor of Arts in Economics from Vassar College, New York. He has a background in Economics, Accounting, Political Science and Operations (Event Management). He is from Hyderabad, India. Prior to Crowd Valley, Adit has worked as a research analyst for Baring's Private Equity Partners in Mumbai and for the IdeaSpace Foundation in Manila as well as a risk analyst for Fincare in Bangalore. On the operations side, Adit has organized and run over 30 large scale events that cater primarily to a college community. He is currently based in New York City.

RSS Feed

RSS Feed