A great disruption is underway in financial services, yet it’s still open who will come out on top in each distinct category of offerings. Will it be the institutions modernizing their fundamental approach to financial services or will it be digital native, technology firms that enter the sector to give clients the service they want?

Ultimately the balance is going to land somewhere in the middle, but looking at both forces in the equation, what we can do is support innovation that challenges the status quo and serves as a true enabler for end users, wherever that innovation might come from.

This is a call for developers, for innovators that are dissatisfied at the status quo in finance, even furious, and want to do something about it. Based on observational data, there are many areas of interest that you can take my word for. But if you’re going for one of these, please do reach out and we will try to find a way to back you long term.

This is a call for developers, for innovators that are dissatisfied at the status quo in finance, even furious, and want to do something about it. Based on observational data, there are many areas of interest that you can take my word for. But if you’re going for one of these, please do reach out and we will try to find a way to back you long term.

Source: Blurred lines: How FinTech shaping Financial Services in Luxembourg by PwC.

Looking for a fintech opportunity? Here are 8:

Business services

1. SME finance is still experiencing a gap in the tune of hundreds of billions annually in the US alone yet this is truly a globally prevalent issue. Creating new ways of accessing capital with a novel element that providers aligned interest, for example leveraging online data or creating dynamic repayments to offer a better product, are sorely needed.

2. Providing lenders a better way to evaluate and price SME debt to be able to offer better products.

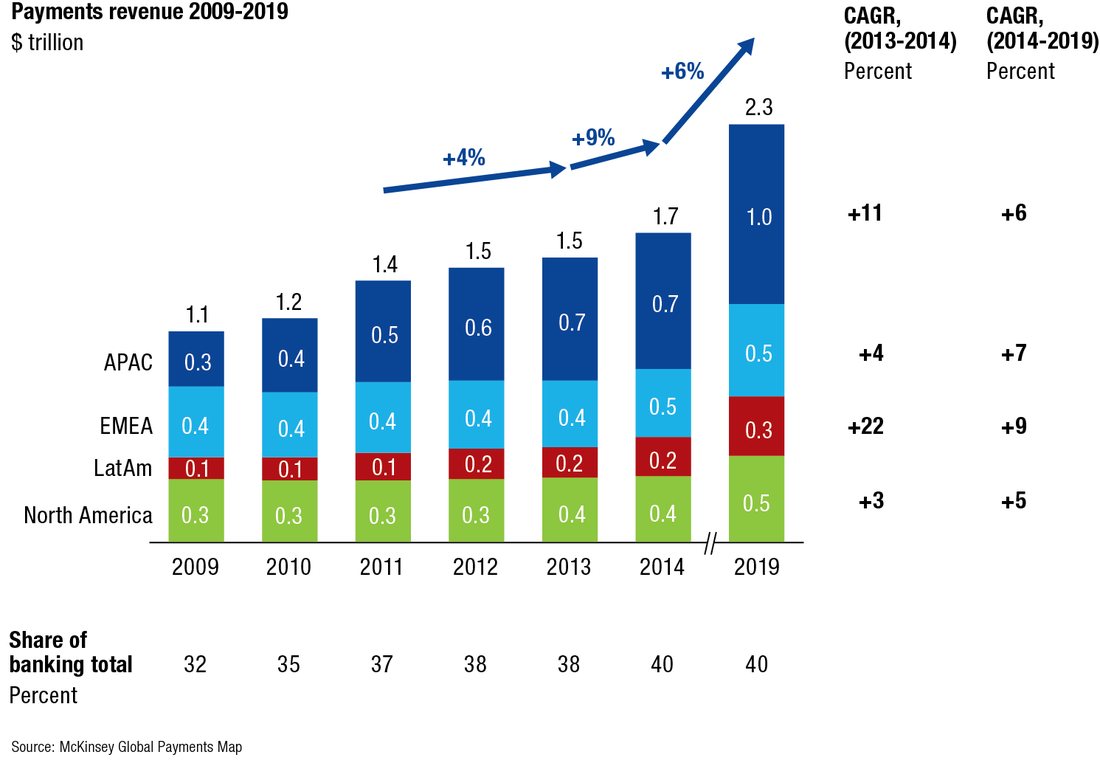

3. Larger payments - Modern and competitive services for the facilitation of larger payments (please kill the check). There is a clear opportunity here, as in the last few years payments revenue have substantially increased their importance as a percentage of the banking total revenue.

Looking for a fintech opportunity? Here are 8:

Business services

1. SME finance is still experiencing a gap in the tune of hundreds of billions annually in the US alone yet this is truly a globally prevalent issue. Creating new ways of accessing capital with a novel element that providers aligned interest, for example leveraging online data or creating dynamic repayments to offer a better product, are sorely needed.

2. Providing lenders a better way to evaluate and price SME debt to be able to offer better products.

3. Larger payments - Modern and competitive services for the facilitation of larger payments (please kill the check). There is a clear opportunity here, as in the last few years payments revenue have substantially increased their importance as a percentage of the banking total revenue.

4. Further ways of identifying and verifying businesses in KYC processes. With an average business onboarding time of around 6 weeks, the more we can introduce supportive tools for the satisfaction of compliance the better service we can expect.

5. Institutional client centricity - digital transformation has become an increasing area of investment the past decade. Yet this digital transformation varyingly ends up at the end consumer level. A customer centric transformation is called for in most financial institutions, are you the champion to start with the little guy and ask what the bank is doing for them?

5. Institutional client centricity - digital transformation has become an increasing area of investment the past decade. Yet this digital transformation varyingly ends up at the end consumer level. A customer centric transformation is called for in most financial institutions, are you the champion to start with the little guy and ask what the bank is doing for them?

Source: Fintech Ranking.

Consumer services

6. Liquidity for retail investors - with the rise of new investment portals into often illiquid securities of varying kind, retail investors in particular are at risk of being locked in for a longer period of time. Providing tools and avenues to alleviate this problem in a responsible way would likely greatly benefit the participants.

7. Fraud prevention tools - the establishment of the sharing economy has brought a lot of data to the surface. With continued exposure of sensitive information, fraud prevention and mitigation becomes an enduring challenge.

Ancillary services

8. Data protection and ownership with inception of PSD2 - who owns your data, especially now as that data includes potentially all of your financial history? We need more solutions that provide ways for users to own their data and make conscious decisions on who else accesses it.

Are you working on one of these areas or do you know exactly the right person? We’d love to hear from you and equip you with the tools to succeed.

Consumer services

6. Liquidity for retail investors - with the rise of new investment portals into often illiquid securities of varying kind, retail investors in particular are at risk of being locked in for a longer period of time. Providing tools and avenues to alleviate this problem in a responsible way would likely greatly benefit the participants.

7. Fraud prevention tools - the establishment of the sharing economy has brought a lot of data to the surface. With continued exposure of sensitive information, fraud prevention and mitigation becomes an enduring challenge.

Ancillary services

8. Data protection and ownership with inception of PSD2 - who owns your data, especially now as that data includes potentially all of your financial history? We need more solutions that provide ways for users to own their data and make conscious decisions on who else accesses it.

Are you working on one of these areas or do you know exactly the right person? We’d love to hear from you and equip you with the tools to succeed.

RSS Feed

RSS Feed