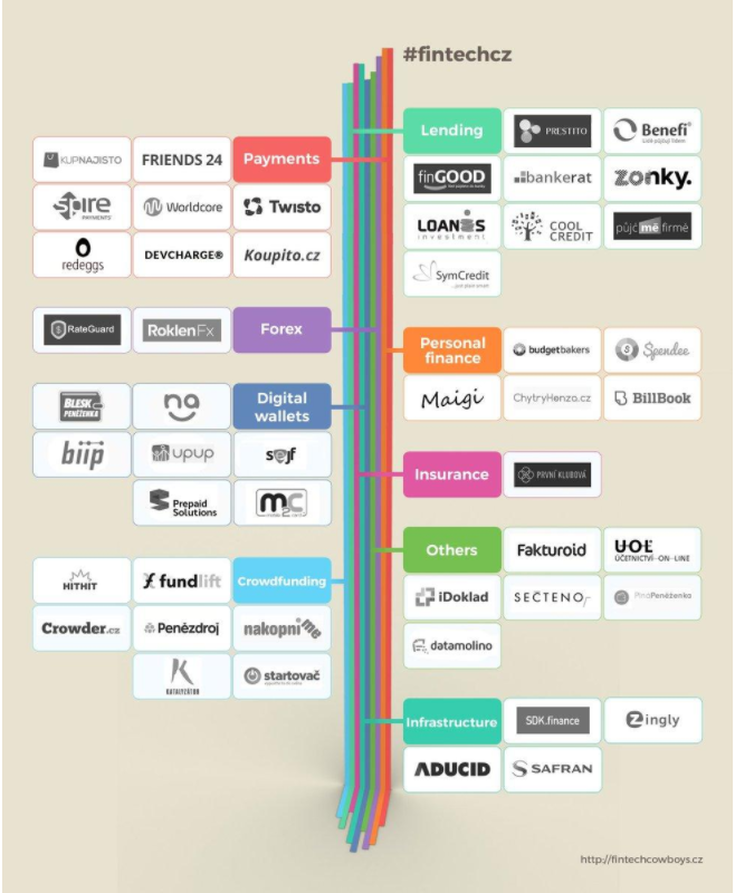

Turning our attention to Eastern Europe, the beautiful country of Czech Republic, steeped in history, catches our attention. With focus of the fintech world concentrated on hubs such as New York, Silicon Valley, London and Berlin, Prague seems to run under the radar for the most part but given that Prague is the fifth most visited city in Europe, it can’t afford to fall behind. Looking at the figure below, we see that there are a number of successful fintech firms comprising the Czech ecosystem.

In 2016, the transaction value in the fintech market amounted to US$4,032m with an expected annual growth rate (CAGR 2016-2020) of 16.5 % resulting in the total amount of US$7,424m by 2020. The market's largest segment is the segment "Digital Payments" with a total transaction value of US$4,020m in 2016. This seems to be a recurring trend given the high level of inefficiencies and outdated technology that occupies this space, essentially inviting new entrants to innovate within the payments sector.

Like Germany, the Czech Republic has a strong engineering infrastructure that exists on both the production and education side, facilitating a culture of innovation and resourcefulness. Czechs have a long-standing engineering history. Under socialism, Czechoslovakia was considered, together with the German Democratic republic, the most technically advanced country in the Soviet bloc. The Czech Technical University in Prague, one of the largest in the country, is also the oldest non-military technical university in Europe.

The university's long tradition of cutting edge science and engineering ensues from the work of many great personalities – including the famous physicist Christian Doppler and renowned engineers such as FJ Gerstner and J Bozek.

Alena Vranova, director of the Czech startup behind the Trezor bitcoin vault, Satoshi Labs, points out that the emergence of bitcoin-related businesses may be partly due to its strong education system, "particularly when it comes to technical training".

Czech Republic jumped onto the virtual currency map in 2014 with an incident where “blackmailers” who claimed that they would release the Ebola virus in the country unless they were paid one million euros in bitcoin. The crisis was averted with no bitcoin disbursed or people injured. One of the reasons that this occurred in the Czech Republic may have been because the profile of bitcoin was elevated in the country when in 2013, the Ministry of Finance of the Czech Republic issued legal guidance for buying and selling bitcoin.

In 2015 the growth of bitcoin in the Czech Republic was recognized by the fact that the country had 112 merchants who accepted bitcoin with nearly half of them in the capital city of Prague. It also had 8 bitcoin ATMs in the country, which made them the 12th most popular country for bitcoin ATMs. This may not sound like much, but the same year, there was only 1 bitcoin ATM in New York City. These statistics gain even greater significance given that as of June, 2015 there were 55,000 bitcoin wallet downloads in a population of 10 million where smartphone penetration is 42% of the population and active internet usage is at 77%. As these figures grow, it would be very interesting to see the development of the virtual currency. In late 2015, the Czech Republic’s version of PayPal called GoPay announced that it was accepting bitcoin for its third-party payment system. This was made possible by cooperation from Bitcoinpay and allowed bitcoin to be accepted by over 2,000 merchants in the country.

Furthermore, the very first mining pool called Slush, was in the Czech Republic in 2010, and it continues to operate today with nearly a million BTC mined since it began. The ability to buy bitcoin in the Czech Republic is now so widespread that a Czech citizen’s options for buying bitcoin rival those for Americans and most Europeans.

The history of the nation also plays a part in its growth and development with the past history of totalitarianism in the country impacting the trust of citizens in the government and public institutions which this lends itself well to appeal of the virtual currency seen by many who view the virtual currency as an attractive proposition believing that less regulation by the government will provide more power and prosperity for businesses and citizens, which correlates with the decentralized and "nationless" perception of bitcoin and virtual currency.

The anti-institutional sentiment is complimented by a strong DIY attitude. There seeming to be a prevailing libertarian sentiment among some cohorts of the population, who challenge the status quo by seeking alternative ways of doing things. On this Vranova adds, “Our nature allows us to find solutions even with very limited resources."There is no secure hardware wallet? Okay, let's create it. There is no solution to decreasing rewards from mining? Do a mining pool."

Petr Žílka, a spokesperson for Parelelni Pollis, a non-profit organisation based in Prague that focuses on the potential sociopolitical impact of new technologies, particularly those based on the idea of decentralization, attributes this attitude to the Czech Republic's communist heritage. He further adds that there is an old Czech custom: “if you don't cheat the state you cheat your family", highlighting the level of confidence in the regulators and a tendency/desire for innovation and alternate paths.

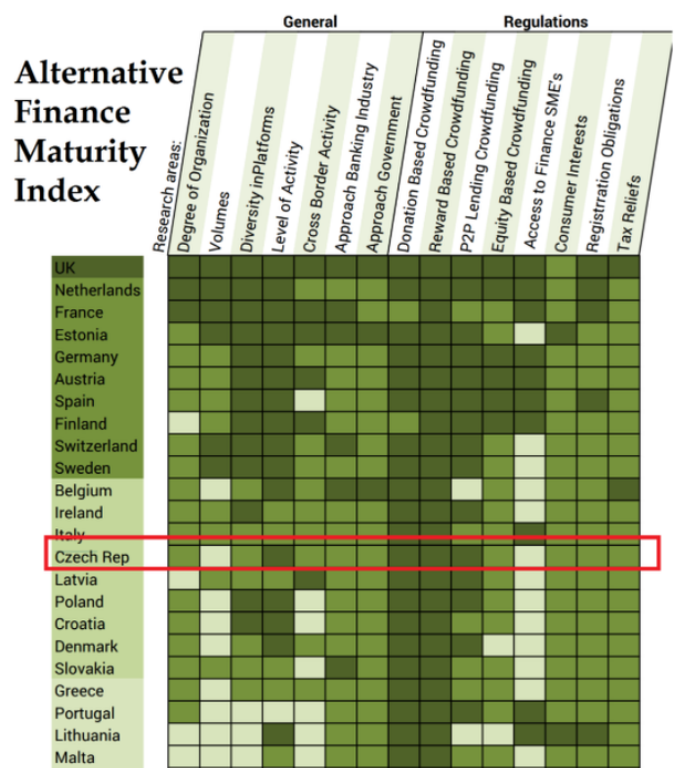

The above figure emphasizes how the Czech Republic is seemingly lacking in the infrastructure for SME Financing making it a prime location for innovation within the nation as well as for international fintechs and entrepreneurs to take initiative and step in to provide accessibility to credit for SME’s thereby boosting overall growth in the country.

As far as crowdfunding in the Czech Republic, the most common form is reward-based crowdfunding, which has existed in the Czech Republic for four years now and is growing every year. For example the Hithit platform raised 80% more money in 2015 than in 2014. The second most used form of crowdfunding in the Czech Republic (that is actually not publically perceived as a form of crowdfunding), is P2P consumer lending. It started to accelerate during 2015 when Zonky.cz was launched. This platform has built its public recognition on the emphasis that people who do not match the criteria of banks should nevertheless have a chance to get a loan. SymCredit and Pujcmefirme represent Czech P2P business lending. These platforms are slowly gaining the trust of the public equity crowdfunding has not been an active form of financing in the Czech Republic so far. Just one campaign has been successfully funded.

Regulation of crowdfunding in the Czech Republic

Czech law does not explicitly regulate crowdfunding, but it does lay down certain rules and limitations for the collection of funds from the public and their use, rules on consumer protection and the prevention of money laundering.

In addition to the general rules establishing consumer protection conditions, including the negotiation of contracts through the internet, regulated by the Civil Code and the Consumer Protection Act, the following Czech laws may be applicable: (i) the Act on Banks, which prohibits the acceptance of deposits from the public without a banking licence; (ii) the Act on Payment Systems, determining rules for the provision of payment services, including transfers of funds; (iii) the Act on Capital Markets, regulating the mediation of investments in shares and bonds and public offerings; (iv) the Act on Public Collections, regulating the collection of voluntary cash contributions from contributors for a predetermined public benefit; and hypothetically also (v) the Lottery Act, where winning or losing is decided by chance.

Whereas those rules are fragmented into many Acts, and it is not always clear which set of rules will apply to each platform, there are many platforms that work outside the statutory regime. Therefore, it would be desirable to adopt a comprehensive regulation laying down rules that are in accordance with the individual sector regulation.

Significant regulatory burden arises, however, in case of equity-based crowdfunding as it remains rather problematic to offer investment stakes in limited liability companies to a crowd of investors in the online environment of crowdfunding marketplaces. In case of equity crowdfunding models, the current environment may require compliance with the provisions of the Act on Banks, the Act on Undertaking Business on the Capital Market, the Act on Bonds or the Act on Investment Companies and Investment Funds.

In order to operate an equity crowdfunding platform, the firm providing the platform may need to be an investment firm (in Czech: “obchodník s cennými papíry”) licensed pursuant to the Act No. 256/2004 Coll., the Capital Markets Act, as amended and meet all the requirements for duly licensed investment firm (the “Investment Firm”), and satisfy further conditions, such as hold a licence for execution of orders concerning investment instruments (e.g. investment securities) on the customer’s account and others.

The total consideration for the investment instruments offered by the platform with respect to each individual project company has to be lower than €1,000,000, otherwise a prospectus must be produced and approved by the respective regulator.

The Czech Ministry of Finance is currently preparing a new Act on Consumer Credits, which will tighten the conditions for the provision and procurement of credits to consumers, probably also including some form of regulation of dedicated crowdfunding platforms for the funding of consumer loans.

Moreover, the EU has long been considering the establishment of harmonised crowdfunding legislation. The European Banking Authority (“EBA“) as well as the European Securities and Markets Authority (“ESMA“) proposed a series of measures to reduce risks connected with crowdfunding, including the possibility of introducing specific registration and regulation of operators of crowdfunding platforms.

It is expected that future EU legislation, which should be presented by the European Commission will resemble the system in the UK, where crowdfunding platforms need to be licensed by the British Financial Conduct Authority.

In terms of disruption and attention by banks, we find that banks have not made any significant steps yet towards becoming an active part in the crowdfunding industry, which might be because they don’t consider it as a real opportunity or threat, yet. One of the Czech branches of Raiffeissen bank tried unsuccessfully to run its own reward-based crowdfunding platform called “Odstartováno”.

Investors have been mostly investing to Czech P2P consumer loans on Bankerat, Benefi or Zonky. Zonky has gained the biggest attention from the investors, as they have several thousand people queuing for investing into the loans on the platform. Investing in loans on the Zonky platform is significantly different from the other platforms because investors have to manually pick each of the projects they want to invest in.

Czech investors are currently also investing on several international P2P platforms as Bondora, Mintos or Twino. The launch of equity crowdfunding platform Fundlist.cz was highly anticipated and since its launch in June, 2016, $760,000 has been raised through public offerings on the platform.

The future is bright for fintech and blockchain in the Czech Republic.

Petr Žílka, a spokesperson for Parelelni Pollis, a non-profit organisation based in Prague that focuses on the potential sociopolitical impact of new technologies, particularly those based on the idea of decentralization, attributes this attitude to the Czech Republic's communist heritage. He further adds that there is an old Czech custom: “if you don't cheat the state you cheat your family", highlighting the level of confidence in the regulators and a tendency/desire for innovation and alternate paths.

The above figure emphasizes how the Czech Republic is seemingly lacking in the infrastructure for SME Financing making it a prime location for innovation within the nation as well as for international fintechs and entrepreneurs to take initiative and step in to provide accessibility to credit for SME’s thereby boosting overall growth in the country.

As far as crowdfunding in the Czech Republic, the most common form is reward-based crowdfunding, which has existed in the Czech Republic for four years now and is growing every year. For example the Hithit platform raised 80% more money in 2015 than in 2014. The second most used form of crowdfunding in the Czech Republic (that is actually not publically perceived as a form of crowdfunding), is P2P consumer lending. It started to accelerate during 2015 when Zonky.cz was launched. This platform has built its public recognition on the emphasis that people who do not match the criteria of banks should nevertheless have a chance to get a loan. SymCredit and Pujcmefirme represent Czech P2P business lending. These platforms are slowly gaining the trust of the public equity crowdfunding has not been an active form of financing in the Czech Republic so far. Just one campaign has been successfully funded.

Regulation of crowdfunding in the Czech Republic

Czech law does not explicitly regulate crowdfunding, but it does lay down certain rules and limitations for the collection of funds from the public and their use, rules on consumer protection and the prevention of money laundering.

In addition to the general rules establishing consumer protection conditions, including the negotiation of contracts through the internet, regulated by the Civil Code and the Consumer Protection Act, the following Czech laws may be applicable: (i) the Act on Banks, which prohibits the acceptance of deposits from the public without a banking licence; (ii) the Act on Payment Systems, determining rules for the provision of payment services, including transfers of funds; (iii) the Act on Capital Markets, regulating the mediation of investments in shares and bonds and public offerings; (iv) the Act on Public Collections, regulating the collection of voluntary cash contributions from contributors for a predetermined public benefit; and hypothetically also (v) the Lottery Act, where winning or losing is decided by chance.

Whereas those rules are fragmented into many Acts, and it is not always clear which set of rules will apply to each platform, there are many platforms that work outside the statutory regime. Therefore, it would be desirable to adopt a comprehensive regulation laying down rules that are in accordance with the individual sector regulation.

Significant regulatory burden arises, however, in case of equity-based crowdfunding as it remains rather problematic to offer investment stakes in limited liability companies to a crowd of investors in the online environment of crowdfunding marketplaces. In case of equity crowdfunding models, the current environment may require compliance with the provisions of the Act on Banks, the Act on Undertaking Business on the Capital Market, the Act on Bonds or the Act on Investment Companies and Investment Funds.

In order to operate an equity crowdfunding platform, the firm providing the platform may need to be an investment firm (in Czech: “obchodník s cennými papíry”) licensed pursuant to the Act No. 256/2004 Coll., the Capital Markets Act, as amended and meet all the requirements for duly licensed investment firm (the “Investment Firm”), and satisfy further conditions, such as hold a licence for execution of orders concerning investment instruments (e.g. investment securities) on the customer’s account and others.

The total consideration for the investment instruments offered by the platform with respect to each individual project company has to be lower than €1,000,000, otherwise a prospectus must be produced and approved by the respective regulator.

The Czech Ministry of Finance is currently preparing a new Act on Consumer Credits, which will tighten the conditions for the provision and procurement of credits to consumers, probably also including some form of regulation of dedicated crowdfunding platforms for the funding of consumer loans.

Moreover, the EU has long been considering the establishment of harmonised crowdfunding legislation. The European Banking Authority (“EBA“) as well as the European Securities and Markets Authority (“ESMA“) proposed a series of measures to reduce risks connected with crowdfunding, including the possibility of introducing specific registration and regulation of operators of crowdfunding platforms.

It is expected that future EU legislation, which should be presented by the European Commission will resemble the system in the UK, where crowdfunding platforms need to be licensed by the British Financial Conduct Authority.

In terms of disruption and attention by banks, we find that banks have not made any significant steps yet towards becoming an active part in the crowdfunding industry, which might be because they don’t consider it as a real opportunity or threat, yet. One of the Czech branches of Raiffeissen bank tried unsuccessfully to run its own reward-based crowdfunding platform called “Odstartováno”.

Investors have been mostly investing to Czech P2P consumer loans on Bankerat, Benefi or Zonky. Zonky has gained the biggest attention from the investors, as they have several thousand people queuing for investing into the loans on the platform. Investing in loans on the Zonky platform is significantly different from the other platforms because investors have to manually pick each of the projects they want to invest in.

Czech investors are currently also investing on several international P2P platforms as Bondora, Mintos or Twino. The launch of equity crowdfunding platform Fundlist.cz was highly anticipated and since its launch in June, 2016, $760,000 has been raised through public offerings on the platform.

The future is bright for fintech and blockchain in the Czech Republic.

About the Author: Adit Vaddi

Adit Vaddi is a business development associate with a Bachelor of Arts in Economics from Vassar College, New York. He has a background in Economics, Accounting, Political Science and Operations (Event Management). He is from Hyderabad, India. Prior to Crowd Valley, Adit has worked as a research analyst for Baring's Private Equity Partners in Mumbai and for the IdeaSpace Foundation in Manila as well as a risk analyst for Fincare in Bangalore. On the operations side, Adit has organized and run over 30 large scale events that cater primarily to a college community. He is currently based in New York City.

Adit Vaddi is a business development associate with a Bachelor of Arts in Economics from Vassar College, New York. He has a background in Economics, Accounting, Political Science and Operations (Event Management). He is from Hyderabad, India. Prior to Crowd Valley, Adit has worked as a research analyst for Baring's Private Equity Partners in Mumbai and for the IdeaSpace Foundation in Manila as well as a risk analyst for Fincare in Bangalore. On the operations side, Adit has organized and run over 30 large scale events that cater primarily to a college community. He is currently based in New York City.

RSS Feed

RSS Feed