At the beginning of March the Financial Conduct Authority (FCA) - i.e. the British financial authority - announced new regulations for peer-to-peer lending and equity crowdfunding, which will start to be effective from April 1st.

|

|

|

At the beginning of March the Financial Conduct Authority (FCA) - i.e. the British financial authority - announced new regulations for peer-to-peer lending and equity crowdfunding, which will start to be effective from April 1st.

In the last couple of years, crowdfunding has emerged in six different continents, as Crowd Valley’s recently published report shows. From USA to France, from Nigeria to Australia, the company has received requests for crowdfunding services and technologies from many countries. But what about China? What is the situation for crowdfunding there? Could a democratic financing mechanism, like crowdfunding, establish itself in the Chinese Republic?

“Driven by technology on the supply side and the financial crisis on the demand side, an investment revolution has begun.”

Andrew Haldane, Executive Director, Bank of England Direct financing, such as equity crowdfunding and P2P lending, as well as capital markets act both as an information bridge and a conduit of financial flows between a large number of investees/borrowers and a large number of investors/lenders who receive a return for their investment. But the similarities already stop there. The design and characteristics of those two marketplaces are profoundly different.  In October 2013, Crowd Valley published a post explaining the current situation regarding securities crowdfunding in France. In fact, at that time, the French Minister of Small and Medium Enterprises had just announced the opening of a public comment period on the proposed regulation for securities crowdfunding. Four months later, the public consultation is officially closed and France has a new regulation for crowdfunding.

An Appealing Alternative for Both Borrowers and Lenders

P2P lending is probably the crowdfunding sector that is growing the fastest. One of the main reason is that the situation, at least in the US, seems to be favorable given that unemployment is low, people are consolidating debt and improving their personal financial balance sheets, while investors are hungry for yields and cash flow every month.  “The Stoneage didn’t end because we ran out of stones” Al Gore

The Oxford English Dictionary defines crowdfunding as “the practice of funding a project or venture by raising many small amounts of money from a large number of people, typically via the Internet”. The crowdfunding industry is evolving and rapidly dispersing across many areas of finance, and institutional investors starting to enter the market. (That actually resulted in the adoption of the term “institutional crowdfunding”).  The SEC has released a set of proposed rules for implementation of Title III of the JOBS Act, FINRA has released proposed forms and rules for the required registration by funding portals and new rules on general solicitation and general advertising have been put into effect.

But where does that leave the market now? Despite the proposals, the Title III crowdfunding market is not open and won’t be for another few months. Furthermore, questions remain as to how navigable that market will be for newcomers and how profitable it will be in the short to medium term.  "Necessity is the mother of innovation" (Unknown)

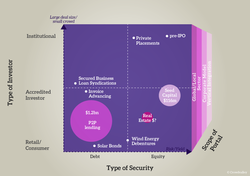

Small and medium-sized enterprises (SMEs) are the backbone of all economies and are a key source of economic growth and technology innovation. They constitute the dominant form of business organisation, accounting for over 95% enterprises globally.  Securities Crowdfunding Market Matrix Securities Crowdfunding Market Matrix “Nothing is as powerful as an idea whose time has come” Victor Hugo

When analysing the crowdfunding market it is typically broken down into four main categories such as donation, reward, debt and equity. Securities crowdfunding, which is the generic clause for debt and equity crowdfunding, is sometimes also called crowdfund investing or crowdfinance. As argued in a previous post, crowdfunding is not a new asset class; it is rather a new conduit for financial flows which dis-intermediates the supply chain of capital allocation, and provides efficiency and transparency in the investment process, enabling investor and issuer to interact in better and more productive ways. In addition it reduces the search cost for the investor and allows for a high degree of risk diversification.  “Crowdfunding platforms could naturally evolve to become the primary source of financial services for young generations” Nathaniel Karp, chief economist for BBVA Research, US Economic Outlook, 2nd Quarter 2013

There is a growing sense that our industrial age capitalism has reached a pivotal point in its evolution. Even people who have long and deep experience of working in the financial system believe it needs change. There is a big mismatch between the financial support today's real economy needs and what financial markets are able to deliver. The banking industry is run by a select few large organisations, which are allowed to create money effectively out of nothing, and which are big lenders to unsustainable sectors such as the coal industry. |

Categories

All

|

RSS Feed

RSS Feed